Managed IT Services for Fintech Startups: What You Need Before You Scale

A fintech startup came to us about eight months after their Series A round. They had been with another MSP that had good reviews online and solid response times. On paper, everything looked fine. But when their compliance team started the SOC 2 audit process, and their security vendor flagged gaps in their endpoint configuration, the MSP's answer was essentially: that's not really our area of expertise.

It turned out that the MSP had built its practice around general SaaS companies and professional services firms. Fintech has different requirements. Not dramatically different in every respect, but different enough that the gaps added up quickly, and by the time this team found us, they were already behind on their audit timeline and dealing with a board that had questions.

We hear versions of this story regularly. Fintech startups move fast, raise capital, sign enterprise customers, and then discover that their IT foundation wasn't built for the scrutiny that comes with financial data. The MSP that worked fine at 15 people starts to feel like a liability at 40.

Here’s what fintech-ready IT support actually looks like.

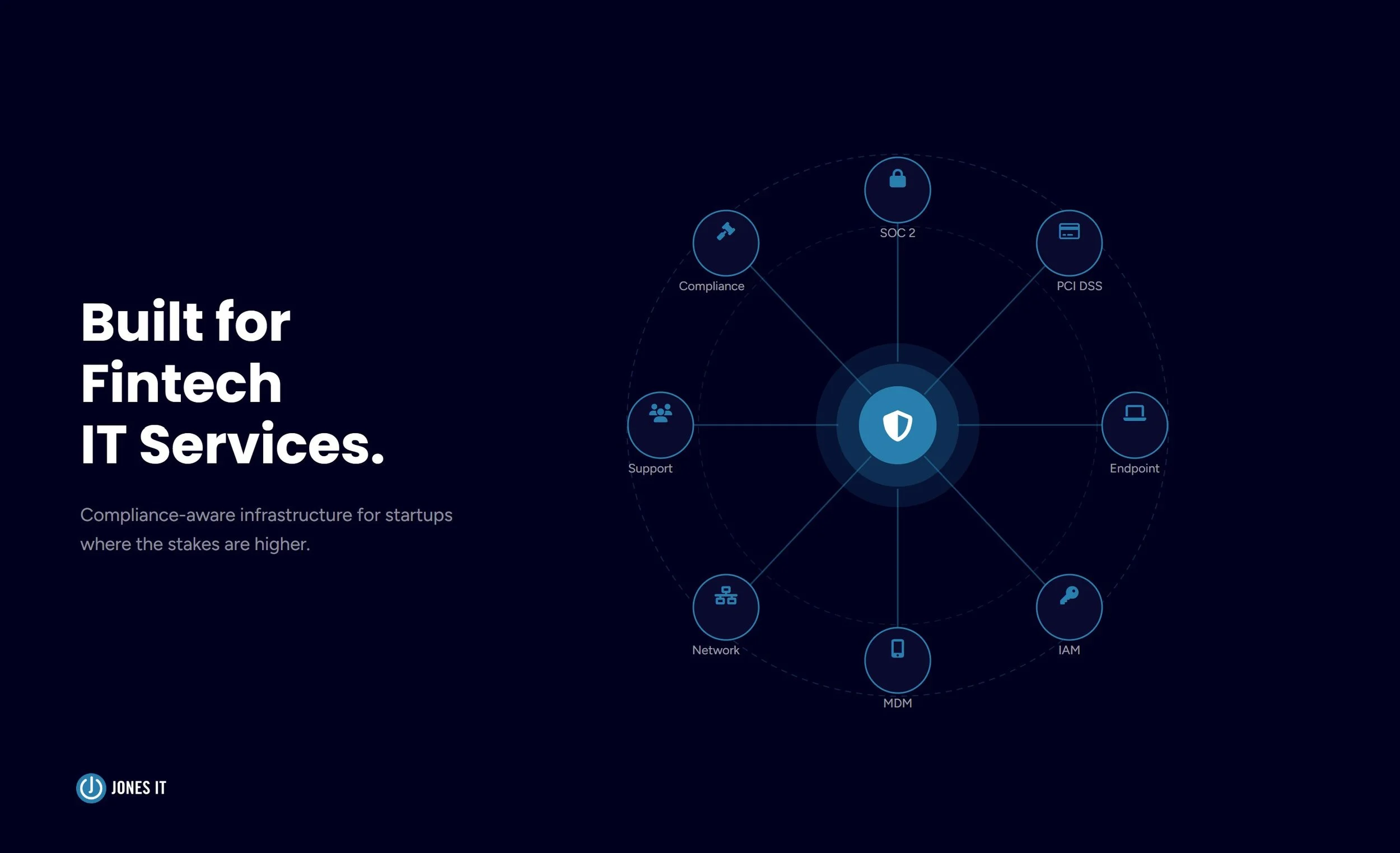

What Fintech Startups Need From IT That General MSPs Miss

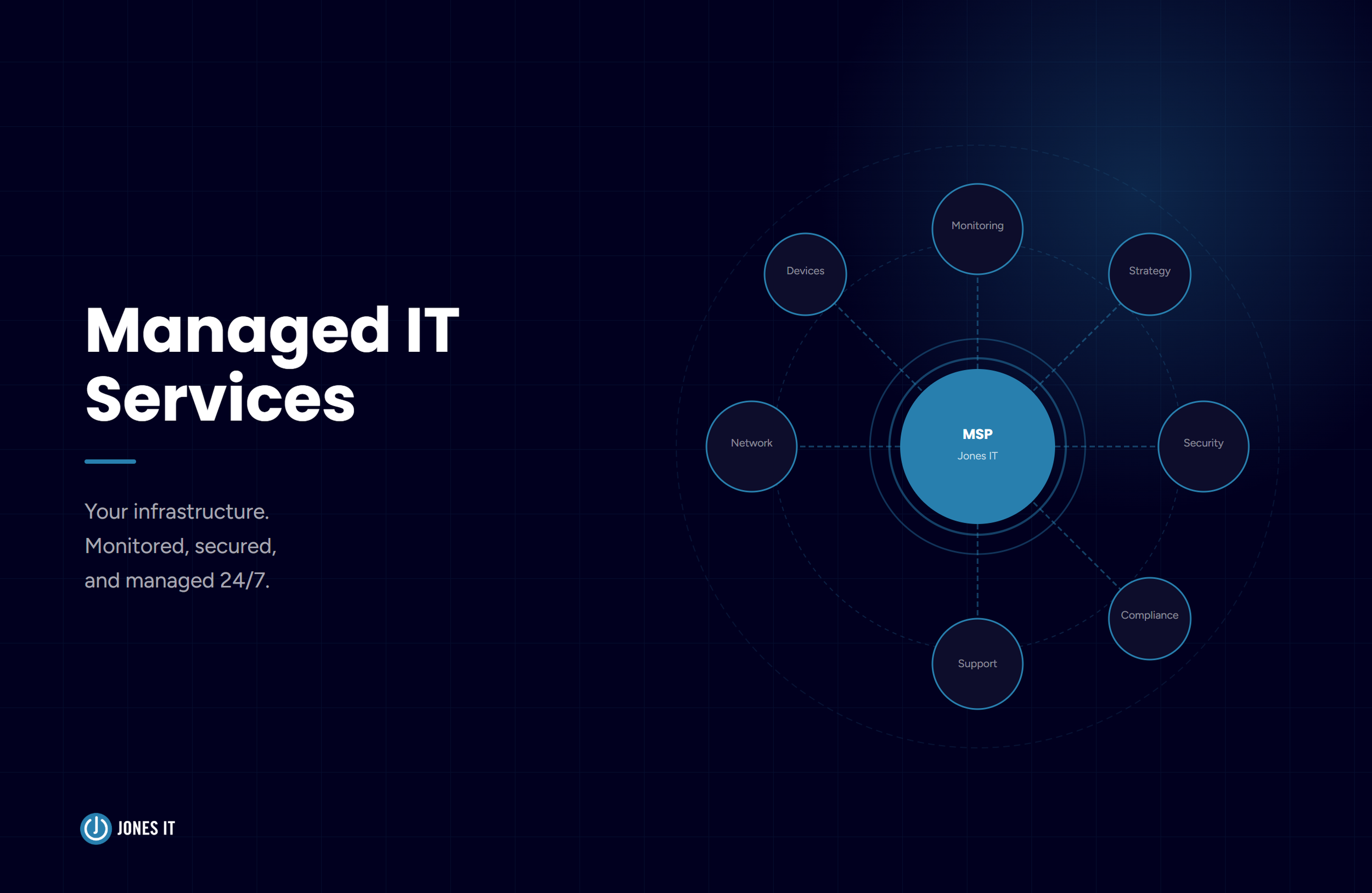

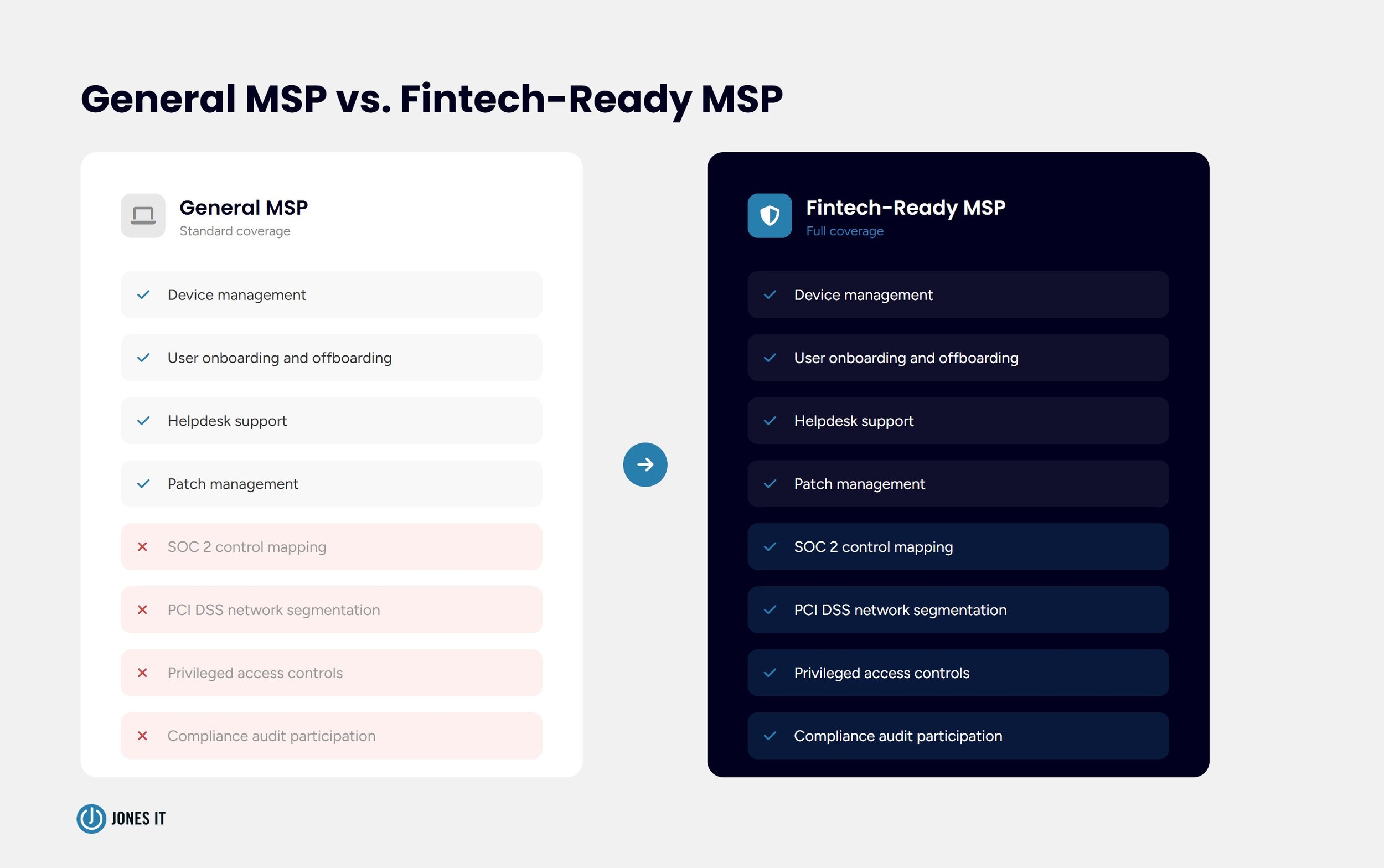

The gap between a general MSP and one that understands fintech runs deeper than technical knowledge. It comes down to familiarity with the compliance frameworks that govern how financial data can be stored, accessed, and transmitted, and the operational habits that keep you audit-ready on a continuous basis rather than scrambling every time a prospect asks for your SOC 2 report. I’ve seen both sides of this, and the difference in day-to-day operations is significant.

Most general MSPs are comfortable with device management, user onboarding, and helpdesk support. Those things matter for fintech companies too. But fintech companies handling payment data, lending workflows, or investment operations carry additional obligations that sit in the intersection of IT and compliance. When your MSP does not understand that intersection, you end up with two separate tracks that do not communicate, and the gaps show up at the worst possible moments: during a security review, a due diligence process, or an audit.

The company that came to us after their Series A had exactly this problem. Their MSP handled devices well, but nobody had mapped their IT configuration to their SOC 2 control requirements. Access controls were inconsistently applied, offboarding procedures had gaps, and their endpoint detection tool was deployed but not centrally monitored: each of these was a manageable issue on its own. But, together, they were a compliance finding waiting to happen.

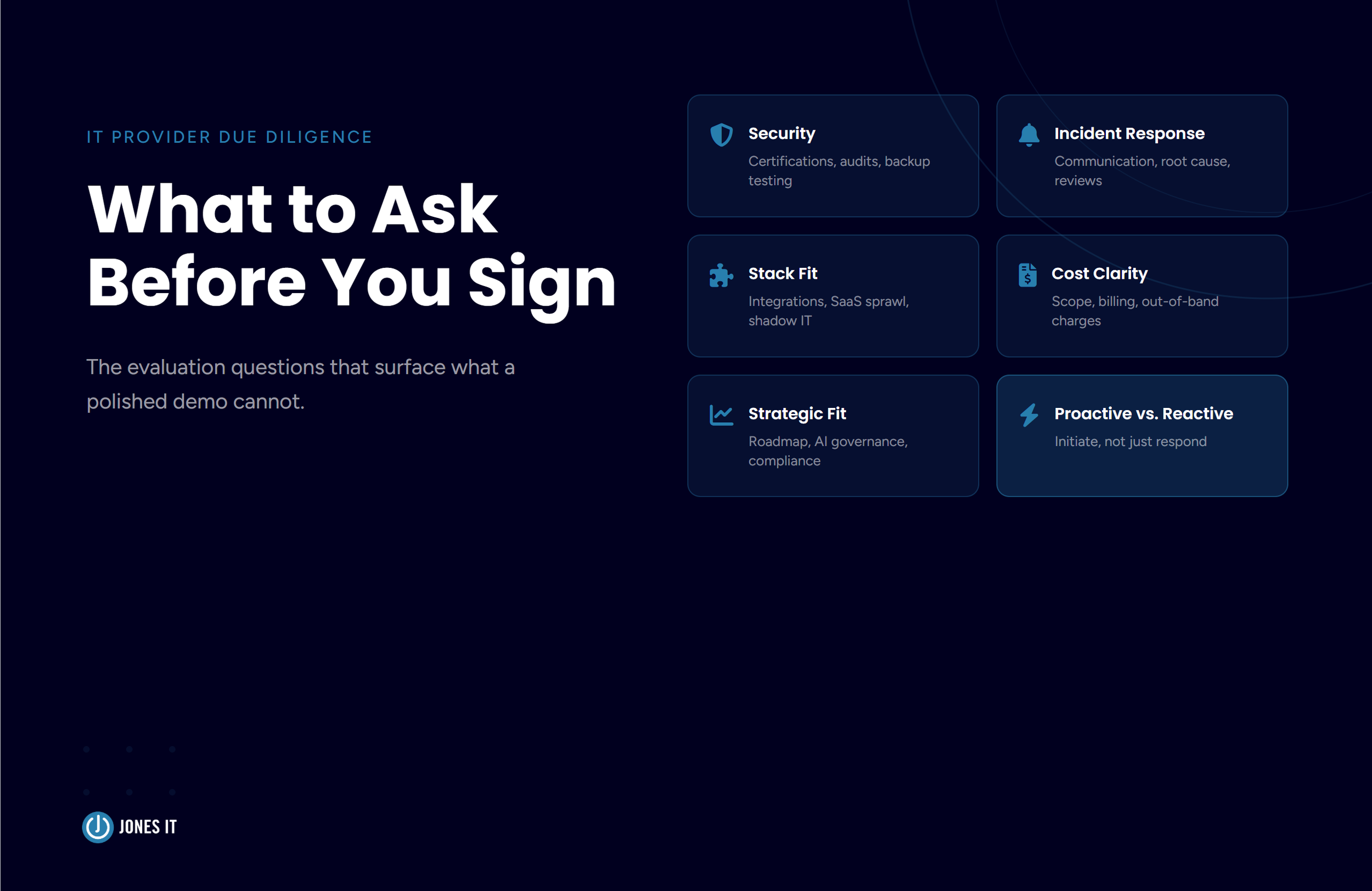

SOC 2 and PCI DSS: The Compliance Stack Fintech Cannot Skip

SOC 2 has become the de facto trust credential for fintech companies selling to enterprise customers or operating in regulated markets. Most Series A and Series B fintech companies will face SOC 2 requirements from at least one customer or investor within their first 18 months of operation. The Type 1 report tells auditors your controls exist, while the Type 2 tells them your controls have held up over time. The IT layer is the basis of both.

What this means practically is that your MSP needs to understand which IT configurations map to which SOC 2 Trust Service Criteria. Logical access controls, endpoint security posture, change management procedures, and incident response plans are all IT functions that directly feed into your audit evidence. An MSP that treats these as separate from compliance is not the right fit for a fintech company, full stop.

For fintech companies handling payment card data, PCI DSS requirements layer on top of SOC 2. The Payment Card Industry Data Security Standard sets specific requirements for how cardholder data environments are configured, segmented, and monitored. Network segmentation that keeps payment processing systems isolated from the rest of your infrastructure is an IT architecture decision with direct compliance implications. Getting it right from the start is significantly cheaper than retrofitting it after the fact.

Here is what your MSP should be doing on the compliance side:

Mapping your IT controls to your SOC 2 Trust Service Criteria from the start, not as an afterthought.

Maintaining audit-ready documentation for endpoint configuration, access provisioning, and offboarding.

Advising on network segmentation for any cardholder data environment, in coordination with your compliance team.

Running regular access reviews so that permissions do not drift over time.

Participating in your annual risk assessment process as an active contributor, not a bystander.

The fintech company we mentioned earlier had none of this in place. Their MSP had never been a part of the compliance conversation. Getting them to SOC 2 readiness required rebuilding several IT processes from scratch while the business was still running at full speed. That is the harder way to do it.

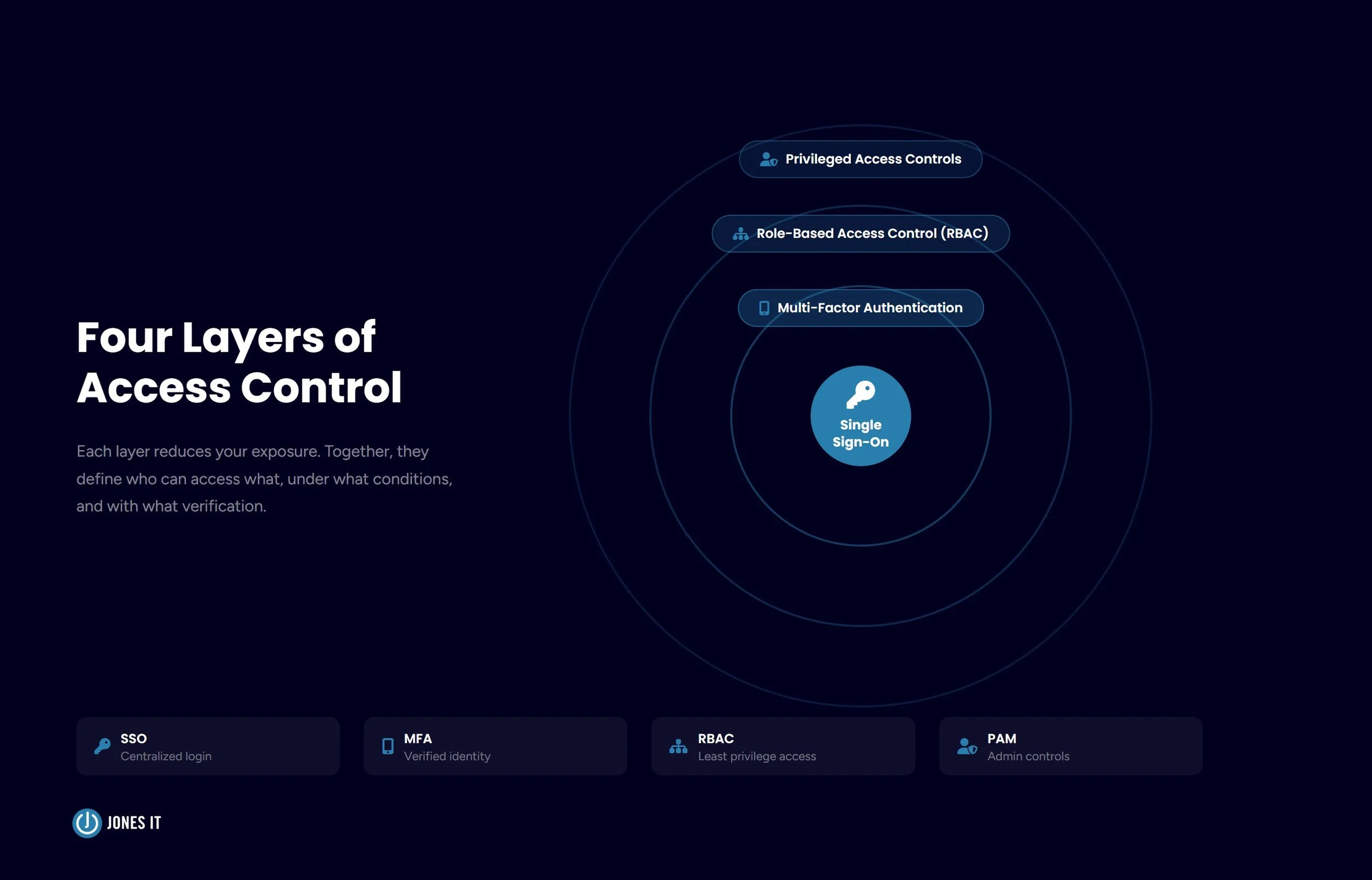

Identity and Access Management in High-Stakes Environments

Identity and access management (IAM) is where a lot of fintech companies have their first serious security incident. Financial systems contain data that is highly valuable to attackers and highly regulated by law. The controls around who can access what, under what conditions, and with what verification are not optional extras; they are core infrastructure.

A well-configured IAM setup for a fintech startup typically covers several things your MSP should be handling directly. Single sign-on (SSO) gives you centralized control over application access. Multi-factor authentication (MFA) is non-negotiable for any system that touches financial data or customer records. Role-based access control (RBAC) means employees only have access to what their role requires, limiting the blast radius if credentials are compromised.

Privileged access deserves its own conversation. Engineers and IT administrators with elevated permissions in your cloud infrastructure or financial systems need additional controls, such as separate privileged accounts, session logging, and regular reviews of what those accounts can actually do. Most fintech companies at the seed and Series A stage have not formalized this yet, which is understandable, but it becomes a finding in almost every SOC 2 audit. Every single time. It is one of those things that feels low-priority until an auditor is sitting across from you, asking for evidence.

The offboarding side of IAM gets less attention but causes real problems. When an employee leaves, access needs to be revoked completely and quickly across every system, including the ones nobody thinks to check. (And there are always ones nobody thinks to check.) An MSP with visibility across your entire application stack can run a complete offboarding checklist. On the other hand, one that only manages your devices will leave gaps.

We recommend fintech companies revisit their IAM posture at every major growth milestone. What works for a 10-person team rarely holds together at 50, and the access patterns that made sense when everyone knew each other can become serious risks when you are onboarding 5 new people a month.

One area worth flagging specifically is third-party access. Fintech companies typically integrate with a range of external vendors, like payment processors, data providers, and banking infrastructure, and each of those integrations creates an access pathway that needs to be managed, monitored, and reviewed. Your MSP should have a view into all of it, internal accounts and vendor connections alike. Vendor access that goes unreviewed for 12 months is a pretty common finding, and not a fun one to have to explain to your auditor.

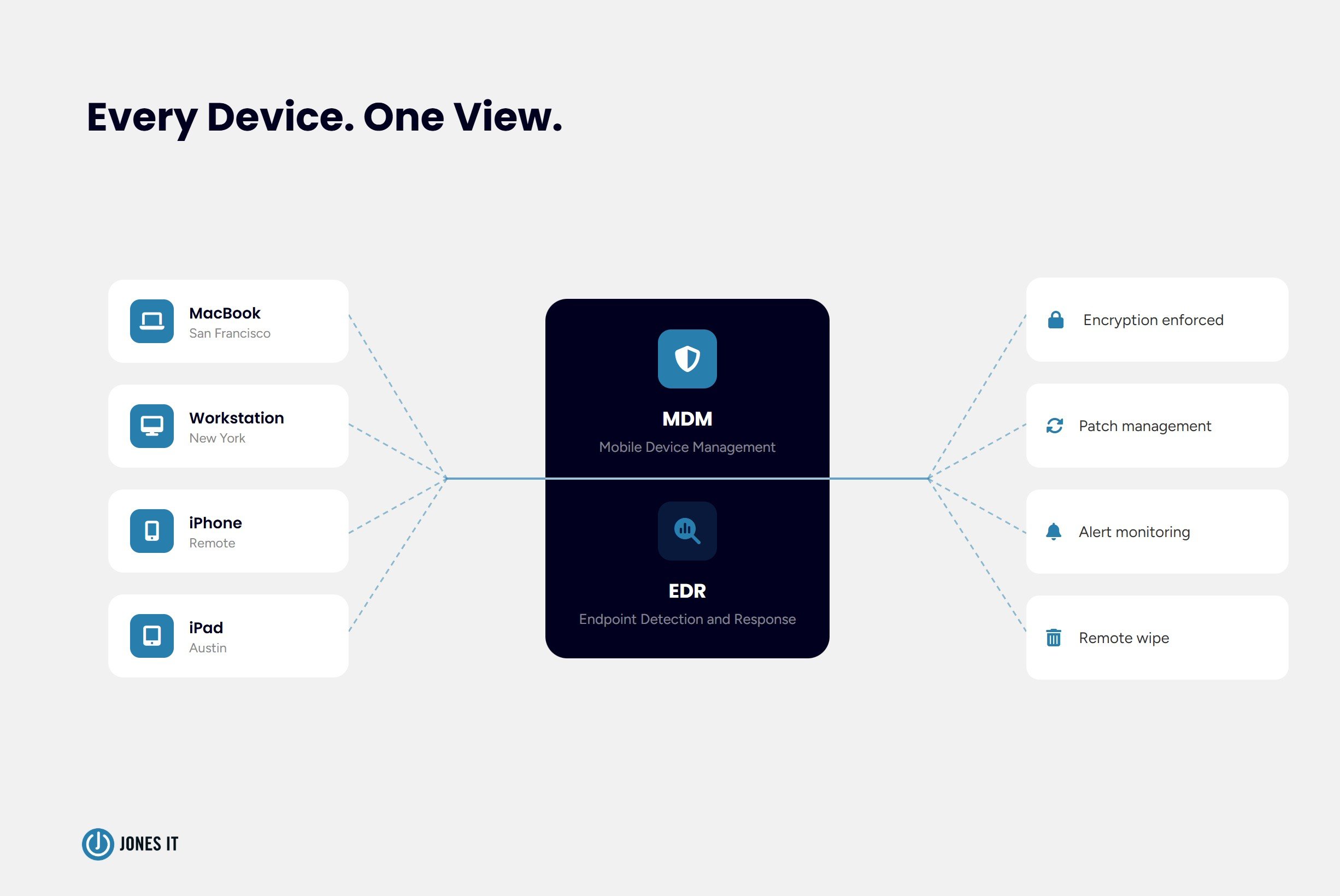

Device Management and Endpoint Security for Distributed Fintech Teams

Fintech teams are usually distributed. Engineers in different time zones, a mix of remote and hybrid work, and a workforce that expects to access company systems from wherever they are. This is fine, but it requires a device management posture that gives you visibility and control without creating friction that makes people route around your security tools.

Mobile device management (MDM) is the foundation. Every company-issued device needs to be enrolled in an MDM platform that lets you enforce encryption, push security policies, deploy software consistently, and wipe a device remotely if it is lost or if someone leaves the company. For fintech companies, this is not optional; it is an expected control in a SOC 2 audit.

Endpoint detection and response (EDR) goes a step further. Where traditional antivirus software looks for known malware signatures, EDR tools monitor behavior and can catch threats that do not match any known pattern. For a fintech startup where a compromised endpoint could mean access to financial systems or customer data, behavioral detection is worth the additional investment.

The catch is that having these tools deployed is different from having them monitored. We see this gap constantly: a company installs an EDR tool, checks the box, and then nobody is watching the alerts. Your MSP should have a defined process for reviewing endpoint alerts and escalating when something looks suspicious. If they cannot describe that process off the top of their head, press on it.

A few things to confirm your MSP is handling:

All company devices are enrolled in MDM with encryption enforced.

EDR is deployed and actively monitored, with a defined escalation process for alerts.

Patch management runs on a defined schedule, with critical patches applied quickly.

A clear process exists for provisioning new devices and decommissioning old ones.

There is visibility into any personal devices accessing company systems, with appropriate controls.

How Jones IT Supports Fintech Startups in the Bay Area

We work with fintech startups across the Bay Area, from seed-stage companies figuring out their first IT foundation to Series B teams preparing for enterprise sales cycles and compliance audits. We’ve supported fintech and crypto innovators like CoinList, Mysten Labs, Mercury, EarnUp, and Bitwave, to name a few. What ties all of it together is treating IT and compliance as one conversation rather than two separate vendor relationships.

When we brought on the company that had outgrown its previous MSP, the first thing we did was a full IT audit mapped against its SOC 2 control requirements. We identified the gaps, built a remediation plan, and ran the technical work in parallel with their compliance team. They completed their Type 2 audit on schedule.

That is what fintech-aware IT support looks like. Your MSP shows up at the compliance planning meeting, not only in the helpdesk queue. Your device management configuration is designed with your audit requirements in mind from day one. Your IAM setup gets reviewed at every growth milestone before the problems surface. It sounds like a lot, but once the foundation is solid, most of this runs in the background, which is exactly how it should be.

If you are a fintech startup evaluating your IT setup, or if you have outgrown your current MSP, reach out to us. We are happy to walk through where you are and what it would take to get your IT foundation ready for the next stage of growth.